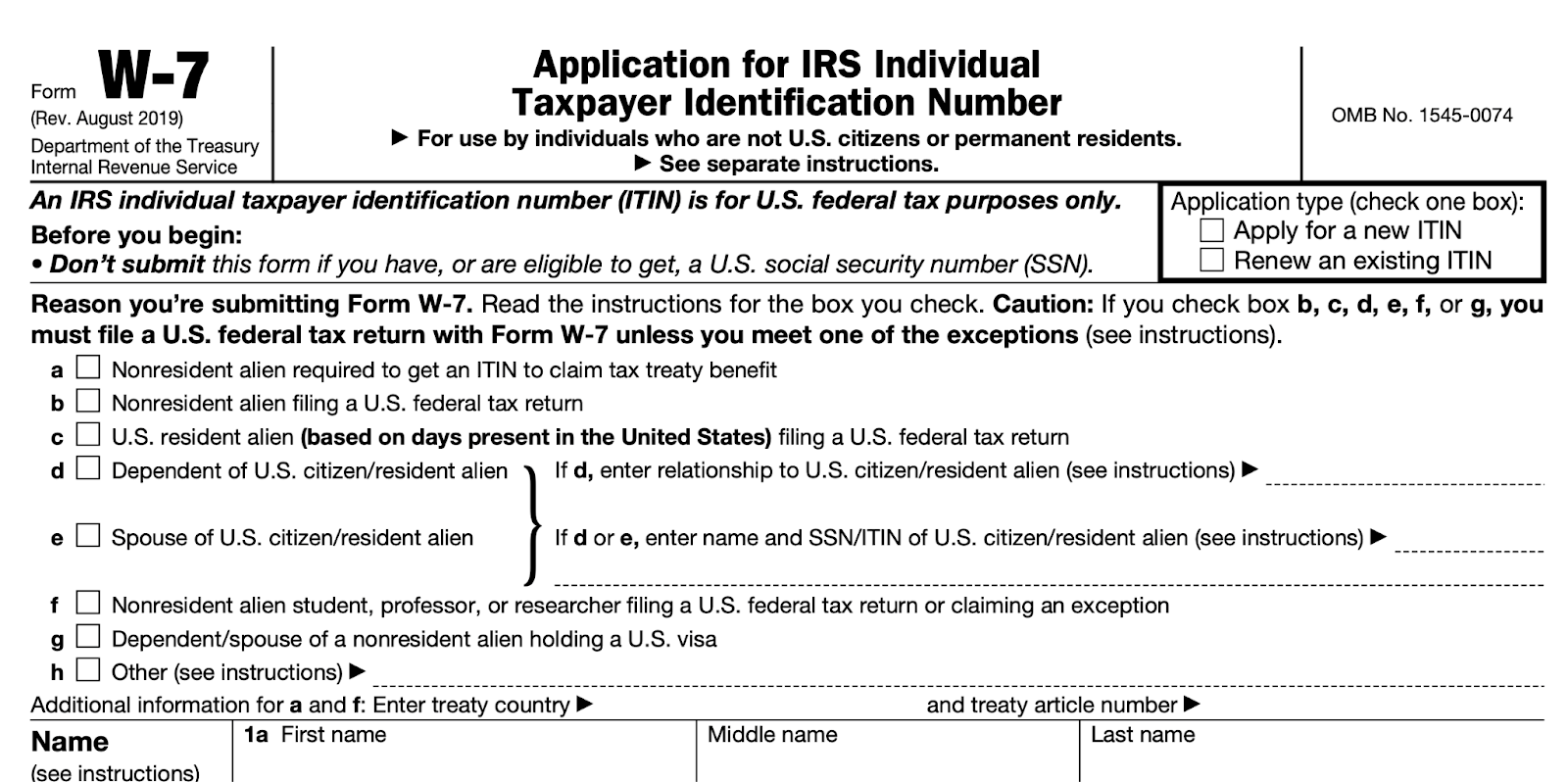

What Is IRS Form W-7 Used For?

IRS Form W-7 is an official IRS form used to obtain an Individual Taxpayer Identification Number.

You typically need form W-7 for filing taxes with the IRS if you’re not a U.S. citizen and either don’t have, or aren’t eligible for, a social security number.

However, it can also be used for:

- Obtaining a mortgage

- Employment settlement disputes

- Opening an interest-bearing checking account

Read on for a quick and easy guide to filling out Form W-7 and obtaining your ITIN.

Do I Need an ITIN?

If you’re not a U.S. citizen or if you can’t obtain a social security number for another reason you must have an ITIN to legally pay taxes on U.S. earnings.

You also may need an ITIN for other reasons, such as applying for an ITIN or opening an interest-bearing checking account.

Can I Fill Out Form W-7 Online?

The short answer is: No, in 2024 you can’t fill out Form W-7 or obtain an ITIN number online.

With that said, be on the lookout for services that claim they can get you an ITIN online.

They’re not helping you obtain an ITIN online but rather digitally obtaining your information when you submit their online form and then physically printing and mailing out your W-7 form for you.

These services can not get you your new ITIN number any faster than you can if you simply fill out the form, print, and mail it yourself (and for much less than what they charge).

How to Fill Out IRS Form W-7(Step-By-Step Instructions)

Unfortunately, the only way to submit Form W-7 and obtain an ITIN is by mail or in person.

However, it’s a simple one-page form that’s pretty self explanatory.

Just make sure to:

- Fill out any and all relevant information, and

- Do not leave any field blank. If a field doesn’t apply to you, write “NA” in the field instead of leaving it empty

Start by downloading the official PDF form here: Form W-7.

Then follow these steps:

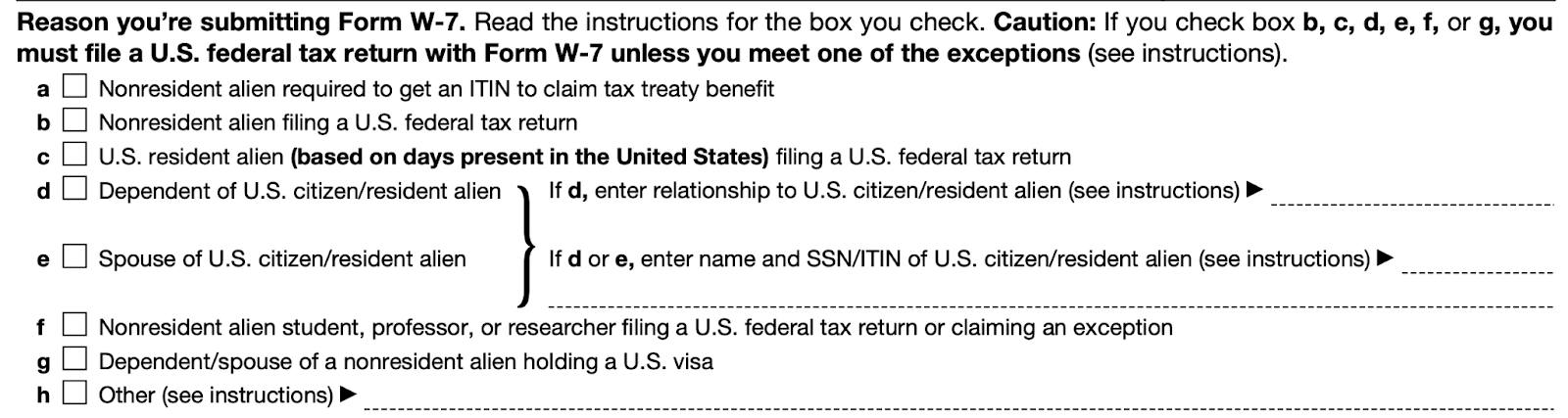

1. Select your reason for submitting

First, start by selecting the reason that you’re submitting Form W-7:

Note that the instructions state that unless your reason is “a” or “h”, you must submit your federal tax return with Form W-7.

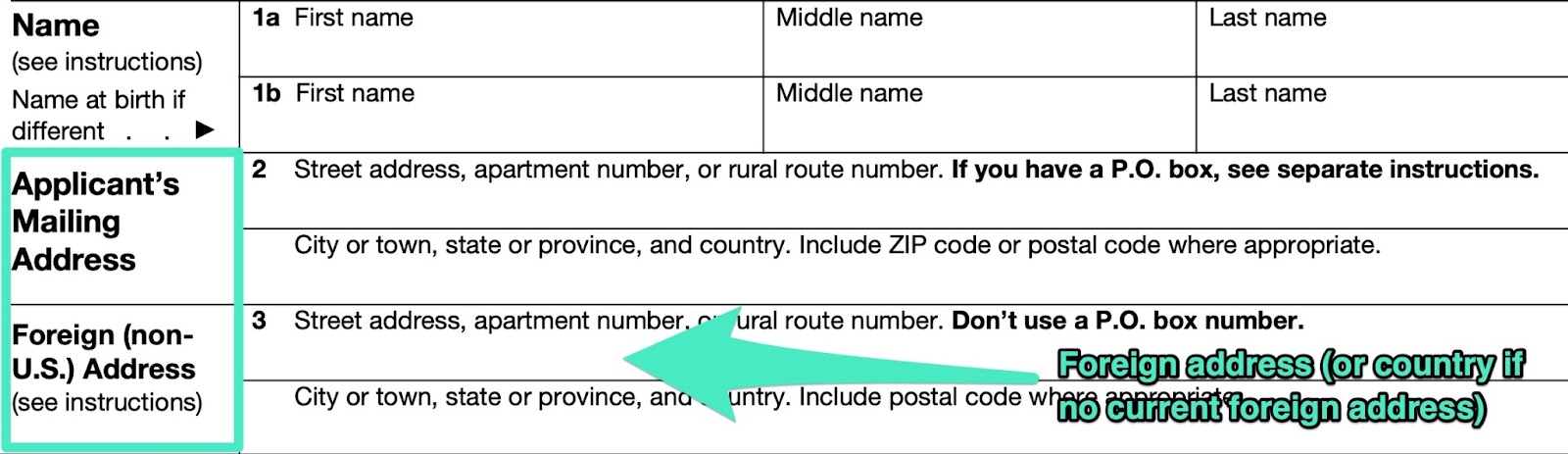

2. Enter your name and address

Next, you’ll fill in your name and one or two addresses.

The first is your current address. The second is your foreign address:

If you no longer have a current foreign address, the place where you resided before coming to the U.S., then you’ll simply fill in the country in which you resided.

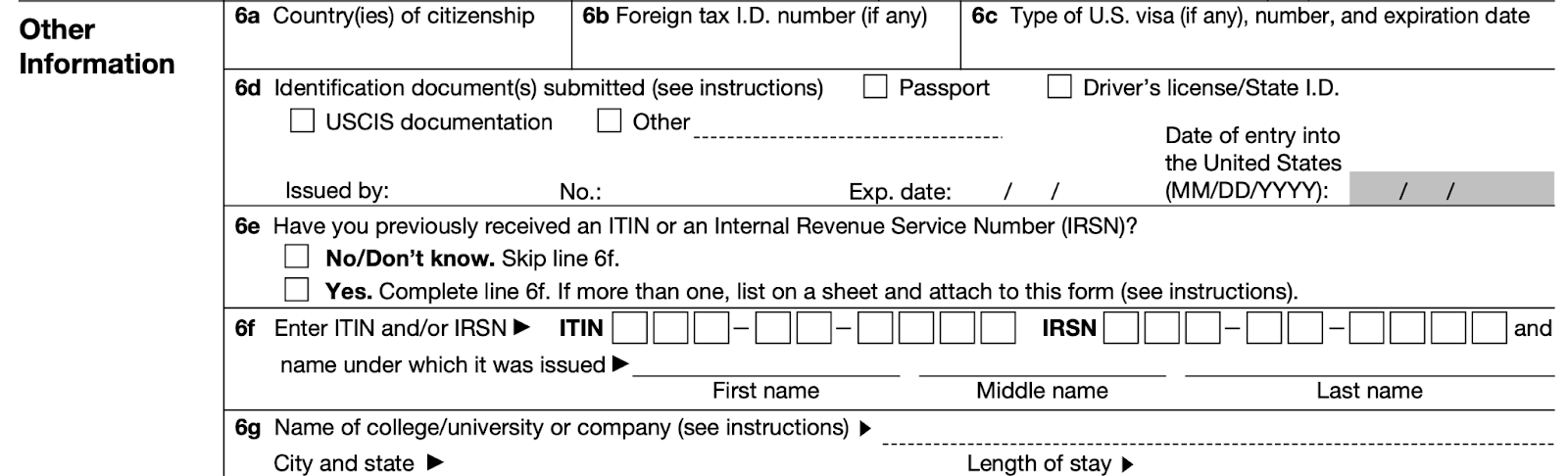

3. Other information

Form W-7 has a whole section for additional information, at least some of which is relevant to you:

Make sure to fill in any and all information that is relevant to you.

Most importantly, notate what identification documents you submitted as well as previous or current countries of citizenship, foreign tax ID numbers, and Visa info (if you have one).

Also, if you’re requesting a new ITIN, fill out sections 6e and 6f.

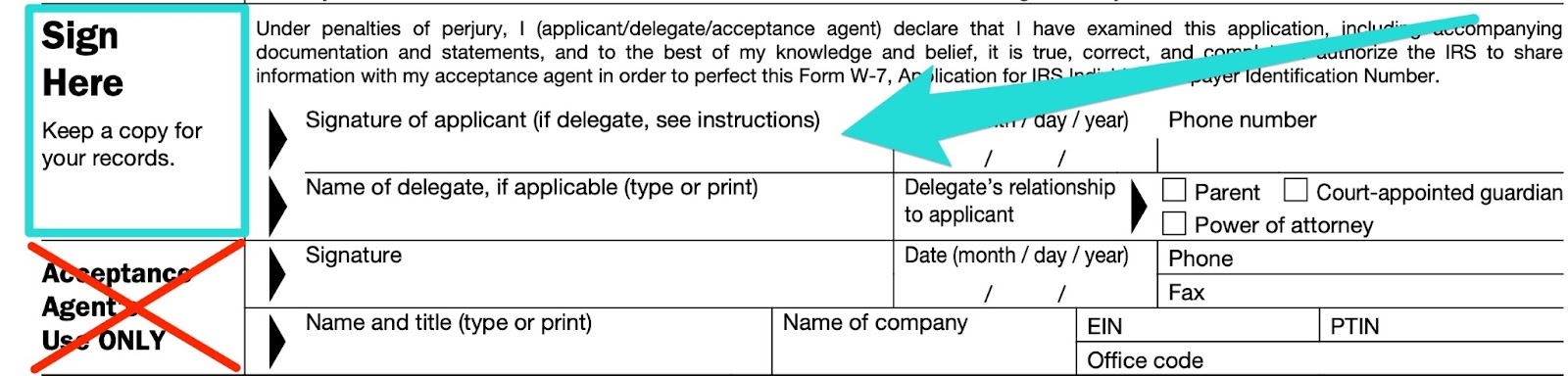

4. Sign and date

Lastly, sign and date your form:

Make sure to sign the top section and ignore the second as that is only relevant if you visit an acceptance agent in person.

3 Ways to Submit Form W-7

While you can’t submit Form W-7 online, there are at least a few options for sending it out, two which allow you to handle it in-person (though the wait time for a response with your new ITIN still applies).

Those methods are:

1. Physical Mail

The first option is simply to mail it yourself.

One of the benefits of Form W-7 is that you can mail it along with your tax return, allowing you to knock out two birds with one stone (at least, if you had planned to physically mail your return).

In order for your form and return to be accepted, you’ll need to mail it along with proof identity, your tax return, and foreign status documents and send to this address:

Internal Revenue Service

Austin Service Center

ITIN Operation

P.O. Box 149342

Austin, TX 78714-9342

Keep in mind that it can take up to 14 weeks to receive your documents back from the IRS, which means you’ll want to use options #2 or #3 if you’ll need them during that window of time.

2. In Person Option 1: Certifying Acceptance Agent

A second option is to apply in-person with a Certifying Acceptance Agent.

This is a good option for anyone who isn’t comfortable having to mail sensitive information such as your proof of identity and foreign status docs.

3. In Person Option 1: Taxpayer Assistance Center (by Appointment)

A final option is to make an appointment at an IRS Taxpayer Assistance Center.

Again, this is also ideal for anyone who isn’t comfortable having to mail sensitive information.

There isn’t much difference between this and an Acceptance Agent, it’s more about what happens to be in your area. Both are viable in-person options.

How to Check the Status of Your W-7 Application

You can call the IRS directly at 1-800-829-1040 to check the status of your application seven weeks after submitting.

How Long Does It Take for the IRS to Process Form W-7

According to official IRS documentation here, the typical wait time to receive a response and obtain your ITIN is 7 weeks during normal periods and up to 11 weeks during peak season from January 15th – April 30th (i.e. tax season).

Looking for Business Funding? Get Funded Fast with Excel Capital

IRS, big banks, traditional financial institutions. They all have one thing in common: complicated paperwork processes and long wait times.

At Excel Capital, we understand how difficult it can be to obtain a traditional business loan, whether via a big bank or financial institution.

Increasingly higher credit requirements, massive qualification hoops to jump through, and low approval odds has made obtaining traditional business funding harder than ever.

We’ve helped thousands of business owners obtain the capital their business needs with a simpler process:

- Short application

- Fast approval time

- Low to no credit options

- And straightforward answers

Apply with Excel Capital today:

Get the capital your business needs without the hassle. Apply for a small business loan with Excel Capital: